Buying a home is one of the most important financial decisions a person can make. For most buyers, purchasing property requires a mortgage loan that allows them to pay for the house over many years. However, choosing the right type of mortgage can significantly affect monthly payments, long-term financial stability, and total interest costs.

Two of the most common mortgage options are fixed-rate mortgage loans and adjustable-rate mortgage loans (ARMs). Each has unique features, advantages, and potential risks. Some borrowers prefer the security of predictable payments, while others choose flexible loans that may offer lower initial interest rates.

Understanding the differences between these mortgage types is essential for making an informed decision. This article provides a detailed comparison of fixed vs adjustable mortgage loans, explaining how they work, their benefits and drawbacks, and which type may be better for different financial situations.

Understanding Mortgage Loans

A mortgage loan is a long-term loan used to purchase real estate. The borrower agrees to repay the lender over a specific period—commonly 15, 20, or 30 years—through monthly payments that include both principal and interest.

The interest rate attached to the mortgage determines how much the borrower will pay in addition to the original loan amount. This interest rate structure is what differentiates fixed-rate mortgages from adjustable-rate mortgages.

In simple terms:

-

A fixed-rate mortgage keeps the same interest rate throughout the loan term.

-

An adjustable-rate mortgage has an interest rate that changes periodically after an initial fixed period.

These different structures influence monthly payments, financial planning, and overall loan costs.

Fixed-Rate Mortgage Loans

What Is a Fixed-Rate Mortgage?

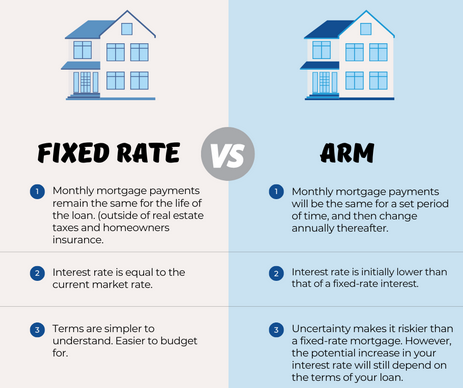

A fixed-rate mortgage is a home loan in which the interest rate remains constant for the entire duration of the loan. Whether the mortgage lasts 15, 20, or 30 years, the borrower pays the same interest rate and similar monthly payments throughout the loan term.

This stability makes fixed-rate mortgages one of the most popular options for homeowners, especially first-time buyers.

Because the rate never changes, borrowers know exactly how much they will pay each month and can plan their finances accordingly.

How Fixed-Rate Mortgages Work

With a fixed-rate mortgage:

-

The borrower agrees to a fixed interest rate at the time of the loan.

-

Monthly payments remain consistent throughout the loan term.

-

Payments are divided between principal (loan amount) and interest.

-

Over time, a larger portion of each payment goes toward the principal balance.

For example, if a borrower obtains a 30-year fixed mortgage at 6% interest, that rate will remain the same regardless of changes in the broader economy or financial markets.

This predictability protects homeowners from fluctuations in interest rates.

Advantages of Fixed-Rate Mortgages

1. Predictable Monthly Payments

The biggest advantage of fixed-rate mortgages is stability. Borrowers pay the same principal and interest each month, making it easier to manage a household budget.

2. Protection from Rising Interest Rates

If market interest rates increase, borrowers with fixed-rate loans are unaffected because their rate is locked in. This protection can save thousands of dollars over the life of the loan.

3. Easier Financial Planning

Because the payment amount never changes, homeowners can plan long-term finances, investments, and savings with greater confidence.

4. Simplicity and Transparency

Fixed-rate loans are easy to understand. There are no complicated rate adjustments or index calculations.

5. Ideal for Long-Term Homeowners

People planning to stay in their homes for many years benefit from stable payments and protection from future rate increases.

Disadvantages of Fixed-Rate Mortgages

1. Higher Initial Interest Rates

Fixed-rate mortgages often start with higher interest rates compared to adjustable-rate mortgages. This means the borrower may pay more initially.

2. Limited Benefit from Falling Rates

If market interest rates decrease, the borrower does not automatically benefit. To take advantage of lower rates, the homeowner must refinance the mortgage.

3. Potentially Higher Monthly Payments

Because the interest rate is usually higher than an ARM’s introductory rate, monthly payments may also be higher during the early years of the loan.

4. Less Flexibility

Fixed-rate mortgages may not be ideal for borrowers who plan to move, sell, or refinance within a short period.

Adjustable-Rate Mortgage Loans (ARMs)

What Is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage (ARM) is a type of home loan in which the interest rate changes periodically based on market conditions.

Unlike fixed-rate loans, ARMs typically start with a lower introductory interest rate for a specific period, after which the rate adjusts according to a financial index.

This means monthly payments may increase or decrease over time.

How Adjustable-Rate Mortgages Work

ARMs usually have two phases:

1. Initial Fixed Period

During the first phase, the interest rate is fixed for several years. Common examples include:

-

5/1 ARM

-

7/1 ARM

-

10/1 ARM

In a 5/1 ARM, the interest rate remains fixed for five years and then adjusts once per year afterward.

2. Adjustment Period

After the initial fixed period, the interest rate resets periodically based on market indexes and lender margins.

When the rate adjusts, monthly mortgage payments may change accordingly.

Advantages of Adjustable-Rate Mortgages

1. Lower Initial Interest Rates

ARMs typically offer lower introductory rates compared to fixed-rate loans, making them attractive to borrowers looking for lower initial payments.

2. Lower Early Monthly Payments

Because the initial interest rate is lower, borrowers usually pay less during the early years of the loan.

3. Potential Savings If Rates Fall

If market interest rates decline, borrowers may benefit from lower monthly payments without refinancing.

4. Ideal for Short-Term Homeownership

People planning to move or refinance before the rate adjustment period may save money with an ARM.

5. Greater Borrowing Power

Lower initial payments may allow borrowers to qualify for larger loan amounts.

Disadvantages of Adjustable-Rate Mortgages

1. Uncertain Future Payments

The biggest disadvantage of ARMs is unpredictability. Monthly payments can increase significantly if interest rates rise.

2. Budgeting Difficulties

Changing payments can make long-term budgeting more complicated for homeowners.

3. Complex Loan Terms

ARMs involve terms such as indexes, margins, and adjustment caps, making them harder to understand than fixed-rate loans.

4. Risk of Payment Shock

When the introductory period ends, borrowers may experience sudden increases in monthly payments.

5. Potential Financial Stress

If interest rates rise dramatically, borrowers may struggle to afford higher payments.

Key Differences Between Fixed and Adjustable Mortgages

Understanding the core differences between these mortgage types can help borrowers choose the most suitable option.

1. Interest Rate Stability

-

Fixed-rate mortgages maintain the same interest rate throughout the loan.

-

Adjustable-rate mortgages change periodically based on market conditions.

2. Monthly Payment Predictability

-

Fixed mortgages provide consistent monthly payments.

-

ARMs may result in fluctuating payments.

3. Initial Interest Rates

-

Fixed mortgages usually start with higher rates.

-

ARMs typically offer lower introductory rates.

4. Risk Level

-

Fixed mortgages carry lower risk because payments remain stable.

-

ARMs involve more risk due to potential interest rate increases.

5. Long-Term Costs

Depending on interest rate trends, either loan type may be cheaper in the long run.

Factors to Consider When Choosing Between Fixed and Adjustable Mortgages

Choosing the best mortgage type depends on several personal and financial factors.

1. Length of Time You Plan to Stay in the Home

Homeowners planning to stay in their property for many years often prefer fixed-rate mortgages for their long-term stability.

However, borrowers planning to move within a few years may benefit from the lower initial rates of ARMs.

2. Interest Rate Environment

Economic conditions play a major role in mortgage decisions.

-

If interest rates are low and expected to rise, locking in a fixed-rate mortgage may be advantageous.

-

If rates are expected to decline, an ARM might offer savings.

3. Financial Stability

Borrowers with stable income and predictable budgets may prefer the certainty of fixed-rate mortgages.

Those with higher income growth potential may accept the risk of adjustable rates.

4. Risk Tolerance

Some borrowers prioritize security and predictability, while others are comfortable with financial risk in exchange for potential savings.

Your comfort level with uncertainty should influence your mortgage decision.

5. Long-Term Financial Goals

Consider how the mortgage fits into your broader financial plans, including:

-

Investments

-

Retirement savings

-

Future home purchases

-

Career changes

A mortgage should support, not hinder, long-term financial stability.

Which Mortgage Option Is Better?

There is no single answer to whether fixed or adjustable mortgages are better. The best choice depends on individual circumstances.

However, certain general guidelines can help.

Fixed-Rate Mortgages Are Better For:

-

Long-term homeowners

-

First-time buyers seeking stability

-

Borrowers with fixed incomes

-

People who want predictable monthly payments

Adjustable-Rate Mortgages Are Better For:

-

Short-term homeowners

-

Real estate investors

-

Borrowers expecting rising income

-

Buyers planning to refinance or sell before the adjustment period

Ultimately, the decision depends on your financial situation, future plans, and comfort with risk.

Real-Life Example

Imagine two buyers purchasing similar homes with different mortgage types.

Buyer A: Fixed Mortgage

-

30-year fixed-rate loan

-

Stable monthly payment

-

Protected from rising interest rates

Buyer A enjoys predictable payments but may pay slightly more initially.

Buyer B: Adjustable Mortgage

-

5/1 ARM with lower starting interest rate

-

Lower monthly payments for the first five years

Buyer B saves money early but faces the risk of higher payments after the rate adjustment.

Both options can be beneficial depending on the homeowner’s plans.

Tips for Choosing the Right Mortgage Loan

When deciding between fixed and adjustable mortgages, consider the following tips:

-

Analyze your long-term housing plans.

-

Compare total loan costs, not just monthly payments.

-

Understand the terms of rate adjustments and caps.

-

Consider future income growth.

-

Consult financial professionals before committing.

Careful evaluation helps ensure the mortgage aligns with your financial goals.

Conclusion

Fixed and adjustable mortgage loans each offer unique advantages and disadvantages. Fixed-rate mortgages provide stability, predictable payments, and protection from rising interest rates. Adjustable-rate mortgages, on the other hand, offer lower initial rates and potential short-term savings but involve greater uncertainty.

The best mortgage choice ultimately depends on factors such as financial stability, homeownership duration, market conditions, and personal risk tolerance.

Borrowers who value security and long-term planning often prefer fixed-rate mortgages, while those seeking lower initial payments or planning short-term homeownership may benefit from adjustable-rate loans.