Buying a home is one of the most significant financial decisions most people make in their lifetime. For many individuals and families, purchasing a home requires obtaining a mortgage loan from a bank or financial institution. However, mortgage approval is not automatic. Lenders carefully evaluate several financial factors before approving a loan, and one of the most important among them is your credit score.

Your credit score serves as a numerical representation of your creditworthiness. It reflects how reliably you have handled borrowed money in the past and helps lenders assess the risk of lending to you. A strong credit score can increase your chances of mortgage approval and help you secure better loan terms, while a poor credit score can make borrowing difficult or more expensive.

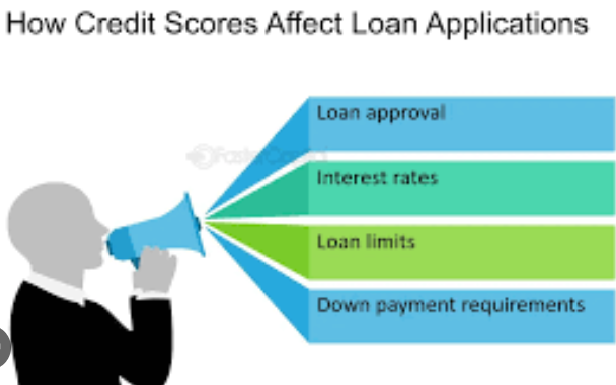

Understanding how credit scores affect mortgage loan approval is essential for anyone planning to buy a home. This article explains what a credit score is, how lenders use it, and the ways it can influence mortgage eligibility, interest rates, and overall borrowing power.

Understanding What a Credit Score Is

A credit score is a three-digit number that represents your financial trustworthiness based on your credit history. It is calculated using information from your credit reports, which track your borrowing and repayment behavior over time.

Credit scores typically range between 300 and 850. The higher the score, the lower the perceived risk to lenders. Borrowers with higher scores are considered more responsible with credit and are therefore more likely to qualify for loans with favorable terms.

Credit scoring models analyze several factors, including:

-

Payment history

-

Amount of debt owed

-

Length of credit history

-

Types of credit accounts

-

Recent credit inquiries

These elements work together to form a comprehensive picture of how well you manage credit. Mortgage lenders use this information to determine whether you qualify for a loan and what interest rate they should offer.

Why Mortgage Lenders Care About Credit Scores

Mortgage loans often involve large amounts of money and long repayment periods, sometimes lasting 15 to 30 years. Because of the financial risk involved, lenders need to ensure that borrowers are capable of repaying the loan consistently over time.

Your credit score helps lenders evaluate this risk. It provides a quick summary of your past financial behavior and predicts how likely you are to repay a loan responsibly.

From the lender’s perspective, borrowers with higher credit scores:

-

Are less likely to miss payments

-

Have a history of managing debt responsibly

-

Pose lower financial risk

As a result, these borrowers are more likely to be approved for a mortgage and offered lower interest rates.

Minimum Credit Score Requirements for Mortgage Approval

Different lenders and loan programs have different credit score requirements. While some mortgages may be available to borrowers with moderate credit scores, better scores generally provide access to more options.

In general terms:

-

Excellent credit scores (740 and above) usually qualify for the best interest rates.

-

Good credit scores (700–739) still receive competitive loan offers.

-

Fair credit scores (620–699) may qualify for many conventional loans but with higher interest rates.

-

Poor credit scores (below 620) may face difficulty qualifying without special loan programs.

Some government-backed mortgage programs allow lower credit scores, but lenders may impose stricter conditions, such as higher down payments or additional documentation.

How Credit Scores Influence Mortgage Interest Rates

One of the most significant ways your credit score affects your mortgage is through the interest rate you receive.

Interest rates determine how much you pay over the life of the loan. Even a small difference in interest rates can significantly increase or decrease the total cost of your mortgage.

Borrowers with higher credit scores typically qualify for lower interest rates because lenders view them as lower-risk borrowers. Conversely, borrowers with lower credit scores often receive higher interest rates to compensate lenders for the increased risk.

For example, a borrower with an excellent credit score may receive a much lower rate compared to someone with a fair or poor credit score. Over the life of a 30-year mortgage, this difference could amount to tens of thousands of dollars in additional interest payments.

The Impact of Credit Scores on Loan Approval Chances

Your credit score directly influences whether a lender will approve your mortgage application. While lenders also consider income, employment stability, and debt levels, credit scores remain a central factor in the approval process.

A strong credit score demonstrates that you have successfully managed loans, credit cards, and other financial obligations in the past. This reassures lenders that you are likely to repay your mortgage on time.

On the other hand, a low credit score may signal potential financial difficulties. Lenders may interpret late payments, defaults, or excessive debt as warning signs. As a result, they may deny the mortgage application or require additional guarantees.

Credit Scores and Down Payment Requirements

Your credit score can also influence how much down payment a lender requires. A down payment is the initial portion of the home’s purchase price that the buyer pays upfront.

Borrowers with strong credit profiles may qualify for mortgage programs that allow lower down payments. Some lenders offer options with down payments as low as 3–5 percent for qualified borrowers.

However, borrowers with lower credit scores may be required to make larger down payments to reduce the lender’s risk. This additional financial commitment can make it more difficult for some buyers to purchase a home.

The Role of Credit History in Mortgage Decisions

While the credit score provides a summary of your creditworthiness, lenders often review your entire credit report during the mortgage approval process.

Credit reports contain detailed information about your financial history, including:

-

Payment patterns on previous loans

-

Credit card balances

-

Past bankruptcies or foreclosures

-

Collection accounts

-

Length of credit relationships

Even if your credit score meets the minimum requirement, certain negative items on your credit report may still affect approval. For example, recent bankruptcies or missed payments may raise concerns for lenders.

Maintaining a consistent record of on-time payments and responsible credit usage can strengthen your mortgage application significantly.

Debt-to-Income Ratio and Credit Score Interaction

Another key factor lenders evaluate alongside credit scores is the debt-to-income ratio (DTI). This ratio compares your monthly debt payments to your monthly income.

A high debt-to-income ratio indicates that a large portion of your income is already committed to paying existing debts. Even with a good credit score, excessive debt may make lenders hesitant to approve a mortgage.

Conversely, a strong credit score combined with a low DTI ratio demonstrates financial stability and increases the likelihood of mortgage approval.

Balancing both factors is essential when preparing to apply for a home loan.

The Effect of Late Payments on Mortgage Approval

Payment history is one of the most influential factors in determining your credit score. Even a single late payment can negatively affect your score and raise concerns for lenders.

Mortgage lenders pay particular attention to recent payment activity. Late payments on credit cards, auto loans, or previous mortgages can signal financial instability.

Multiple late payments within a short period may significantly reduce your chances of loan approval. Therefore, maintaining consistent and timely payments is critical for protecting your credit profile.

Credit Utilization and Mortgage Readiness

Credit utilization refers to the percentage of your available credit that you are currently using. High credit utilization can lower your credit score and suggest that you rely heavily on borrowed money.

For example, if your credit card limits total $10,000 and you have balances totaling $8,000, your utilization rate is 80 percent, which is considered high.

Lower utilization rates generally improve credit scores and demonstrate responsible credit management. Many financial experts recommend keeping utilization below 30 percent when preparing for a mortgage application.

Reducing outstanding balances before applying for a mortgage can help improve both your credit score and overall financial profile.

How Long Credit History Matters

The length of your credit history also plays an important role in determining your credit score. Lenders prefer borrowers who have demonstrated responsible credit behavior over a long period.

A longer credit history provides more data about how you manage debt and financial obligations. This allows lenders to make more confident lending decisions.

Individuals with limited credit histories may still qualify for mortgages, but they may face additional scrutiny or need to provide more documentation regarding their financial stability.

Improving Your Credit Score Before Applying for a Mortgage

If you are planning to purchase a home, improving your credit score before applying for a mortgage can significantly increase your chances of approval and help you secure better loan terms.

Several strategies can help strengthen your credit profile:

Pay all bills on time. Consistent payment history is one of the most important factors in maintaining a strong credit score.

Reduce existing debt. Paying down credit card balances and other loans lowers your credit utilization and improves your financial standing.

Avoid opening new credit accounts. Applying for multiple credit accounts in a short period can temporarily lower your credit score.

Review your credit report regularly. Checking your report allows you to identify errors or inaccuracies that may negatively affect your score.

Maintain older credit accounts. Keeping long-standing credit accounts open helps preserve your credit history length.

Taking these steps months or even a year before applying for a mortgage can make a substantial difference.

How Mortgage Lenders Evaluate Overall Credit Risk

Although credit scores are extremely important, lenders evaluate your entire financial profile when deciding whether to approve a mortgage.

This assessment typically includes:

-

Employment history

-

Income stability

-

Savings and assets

-

Existing debt obligations

-

Credit history

A borrower with a moderate credit score but strong income and low debt may still qualify for a mortgage. Similarly, a borrower with an excellent credit score but unstable income may face challenges.

Mortgage approval ultimately depends on the combination of all these factors.

Special Mortgage Programs for Lower Credit Scores

Some borrowers with lower credit scores may still qualify for specialized mortgage programs. These programs are often designed to help first-time homebuyers or individuals with limited credit history.

Such programs may offer:

-

Lower credit score requirements

-

Smaller down payments

-

Flexible qualification standards

However, these loans may come with additional costs such as higher interest rates or mortgage insurance. Borrowers should carefully evaluate the long-term financial implications before choosing such options.

Long-Term Financial Benefits of a Good Credit Score

Maintaining a strong credit score provides benefits that extend far beyond mortgage approval. A good credit score can help you secure better financial opportunities throughout your life.

These benefits may include:

-

Lower interest rates on loans

-

Easier approval for credit cards

-

Better rental opportunities

-

Lower insurance premiums in some cases

When it comes to homeownership, a higher credit score can translate into significant savings over the life of your mortgage loan.

Preparing Your Credit for Future Homeownership

Planning ahead is one of the most effective ways to ensure mortgage approval. Improving and maintaining your credit score should be a long-term financial goal rather than a last-minute effort.

Potential homebuyers should begin reviewing their credit profiles well before they intend to apply for a mortgage. Building good financial habits, reducing debt, and maintaining consistent payment history can gradually improve credit scores over time.

These proactive steps not only increase the likelihood of loan approval but also help borrowers secure more affordable mortgage terms.

Conclusion

Your credit score plays a crucial role in determining whether you will be approved for a mortgage loan and what terms you will receive. Lenders rely heavily on credit scores to assess risk, evaluate repayment reliability, and determine appropriate interest rates.

A higher credit score increases the chances of mortgage approval, lowers borrowing costs, and expands the range of available loan options. Conversely, a lower credit score may lead to higher interest rates, stricter loan conditions, or even loan denial.

Understanding how credit scores influence mortgage decisions allows prospective homebuyers to take control of their financial future. By maintaining responsible credit habits, reducing debt, and monitoring credit reports, individuals can improve their creditworthiness and strengthen their chances of successfully securing a home loan.